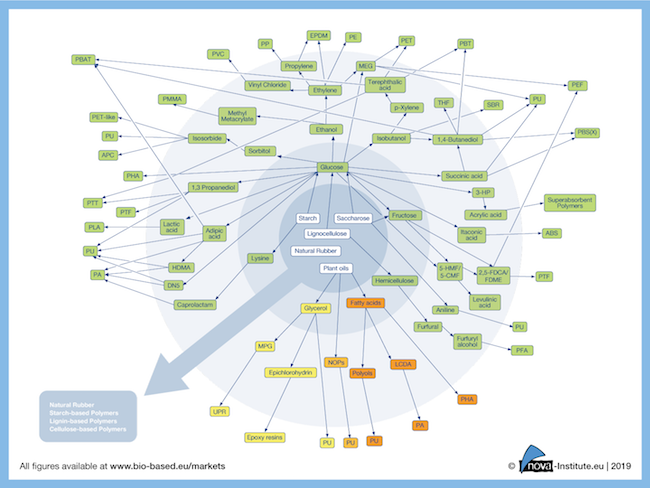

In 2018, the total production volume reached 7.5 million tonnes, representing 2% of the production volume of petrochemical-based polymers. The potential for these materials is currently hampered by low oil prices and a lack of political support, according to nova-Institute.

The production of bio-based polymers has become much more professional and differentiated in recent years, said the report’s summary. “By now, there is a bio-based alternative for practically every application. The capacities and production of bio-based polymers will continue to grow with an expected CAGR of about 4% until 2023, almost at about the same rate as petrochemical polymers and plastics. Therefore, the market share of bio-based polymers in the total polymer and plastics market will remain constant at around 2%.

The increase is mainly a result of the expansion of polylactic acid (PLA) production in Thailand and polytrimethylene terephthalate (PTT) and starch blends production in the United States. New capacity for bio-based polyamides, polyethylene (PE) and, for the first time, polypropylene (PP) and polybutylene adipate-co-terephthalate (PBAT) will be added in Europe during the report’s timeframe. The great biopolymer hope, polyethylene furanoate (PEF), will only be available in commercial quantities after 2023, said nova-Institute.

So far, the two major advantages of bio-based polymers have not been politically rewarded, said the research organization. The first advantage is that bio-based polymers are renewable, which is indispensable for a sustainable plastic industry, the report’s summary noted. The second, which is offered by about a quarter of bio-based polymer production, is biodegradability. Only a few countries—Italy, France and, in the future, probably Spain—will politically support this additional disposal path.The most important market drivers in 2018 were brands seeking to offer customers environmentally friendly solutions and consumers looking for alternatives to petrochemicals. If bio-based polymers were accepted as a solution and promoted in a similar way to biofuels, annual growth rates of 10 to 20% could be anticipated, according to nova-Institute. If the price of oil rises significantly, bio-based polymers could gain market share in similar numbers.

RELATED ARTICLES

- What are Bioplastics and Biopolymers?

- Bioplastics Brands

- Bioplastics Awards

- What is the Difference Between Biodegradable, Compostable and OXO Degradable?

- The History and Most Important Innovations of Bioplastics

- What are Drop-In Bioplastics?

- History of Cellophane

- The History of Elephant Grass Bioplastics

- Bioplastics Companies

- Top Bioplastics Producers

- Polylactic acid or polylactide (PLA)

- What is Bio-BDO?

- McDonalds and the Polystyrene Connections

- The Future of Polystyrene

- Bioplastic Feedstock 1st, 2nd and 3rd Generations

- Palm Oil and The Bioplastics Industry

REFS

This article was published on plasticstoday.com and written by Clare Goldsberry